Inheritance Tax and Pensions when unmarried

The 26th November Budget delivered several key announcements that will affect Financial Planning. Most notably, after a recent consultation period on the Government’s proposals, we now know that from 6 April 2027 pensions will no longer be exempt from IHT.

With pensions being included in the estate from April 2027 this could make estate planning for unmarried individuals even more challenging, especially as the spousal exemption won’t apply.

If you are not married or in a civil partnership, inheritance tax (IHT) could apply on the first death even if you leave everything to your partner, and even if you have been a couple for many years

During lifetime, gifts to a spouse or civil partner would be free from IHT but, again, this exemption would not apply to unmarried couples. The ability to pass on any unused nil rate band or residence nil rate band does not apply to unmarried individuals either.

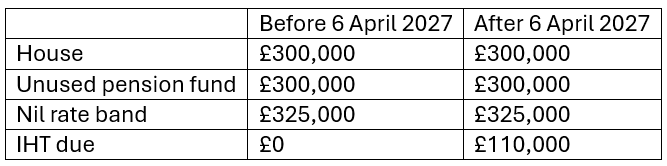

Most people’s main assets will be their house and their pension. Let’s look at how IHT would apply for an unmarried individual if they died before or after April 2027. In this example we have assumed that there are no direct descendants to pass the house to, and therefore the residence nil rate band will not be available.

| Before 6 April 2027 | After 6 April 2027 | |

| House | £300,000 | £300,000 |

| Unused pension fund | £300,000 | £300,000 |

| Nil rate band | £325,000 | £325,000 |

| IHT due | £0 | £110,000 |

In this example there is a significant difference when pensions are included in the estate for IHT, which is made worse by no spouse exemption or residence nil rate band being available.

{kind=link}

It’s also worth remembering that the nil rate band of £325,000 will remain at this level until 2031, which will likely see increased numbers of people in scope of IHT as asset values rise.

If death occurs after age 75, there will also be income tax payable by the beneficiary when they take the benefits from the remaining pension fund after the portion relating to IHT has been deducted.

Ensuring beneficiary drawdown is available, irrespective of when death occurs, could mean less income tax is paid as the beneficiary can control how and when income tax is paid rather than when it is taken as one lump sum.

Potential strategies for unmarried individuals

Lifetime gifts. Make use of the available exemptions. If a gift is exempt, it means IHT will not apply regardless of when you die. The main ones are the annual exemption of £3,000, gifts of up to £250 to any number of people, regular gifts out of surplus income and gifts to charities.

If you make a gift which doesn’t come under any of the exemptions and survive for seven years after making the gift, it will also not be included in the estate.

Think about marriage or civil partnership. In our case study we have seen how this could be beneficial from an IHT perspective, though this may not suit everyone.

Protection policies. A life insurance policy written in trust can provide funds to cover the inheritance tax bill, ensuring the surviving partner is not forced to sell a home to pay the tax.

A joint life annuity. If you are living as a couple but aren’t married or in a civil partnership this might be worth considering. This is because IHT won’t apply to the survivor’s benefit.

Being unmarried can result in significant inheritance tax liabilities that married couples and civil partnerships do not face. Understanding the rules and planning ahead is essential to ensure assets pass on with as little tax as possible.

Making use of the available exemptions, considering a joint life annuity or a protection policy written in trust could be very worthwhile strategies if marriage or a civil partnership is not suitable.

If you have any questions about your inheritance tax or pensions, please do get in touch:

Andrew Smith andrew@michaelforward.co.uk 01908 504083

Michael Forward michael@michaelforward.co.uk 01604 635 435